Final expense insurance is typically a smaller whole life policy designed to cover funeral, burial, and end-of-life costs. Traditional whole life insurance can provide larger lifelong coverage and cash value, but often involves more underwriting and higher premiums. The right fit depends on budget, health, coverage goal, and family needs.

What this search is really asking

People searching for final expense vs whole life insurance are rarely looking for a vocabulary lesson. They are trying to fix a business leak: slow response, weak routing, messy follow-up, unclear compliance state, or a dashboard that hides the real bottleneck. That is why this page treats the keyword as an operating problem, not a content topic.

Searchers compare final expense and whole life because they want protection without being trapped in product jargon. The content needs to clarify purpose before price. For families comparing senior life insurance options, the practical question is whether the system can turn intent into a clean next step before the opportunity gets cold. In 2026, that means the CRM, AI layer, human handoff, and reporting loop need to behave like one system.

Two concrete facts shape the work: Medicare sign-up timing can depend on a person's exact situation, and insurance outreach needs consent, opt-out, and documentation discipline before automation scales. The right build is not louder automation. It is a smaller number of well-controlled moves that create visibility: who came in, what they need, who owns the next step, and whether the next step happened.

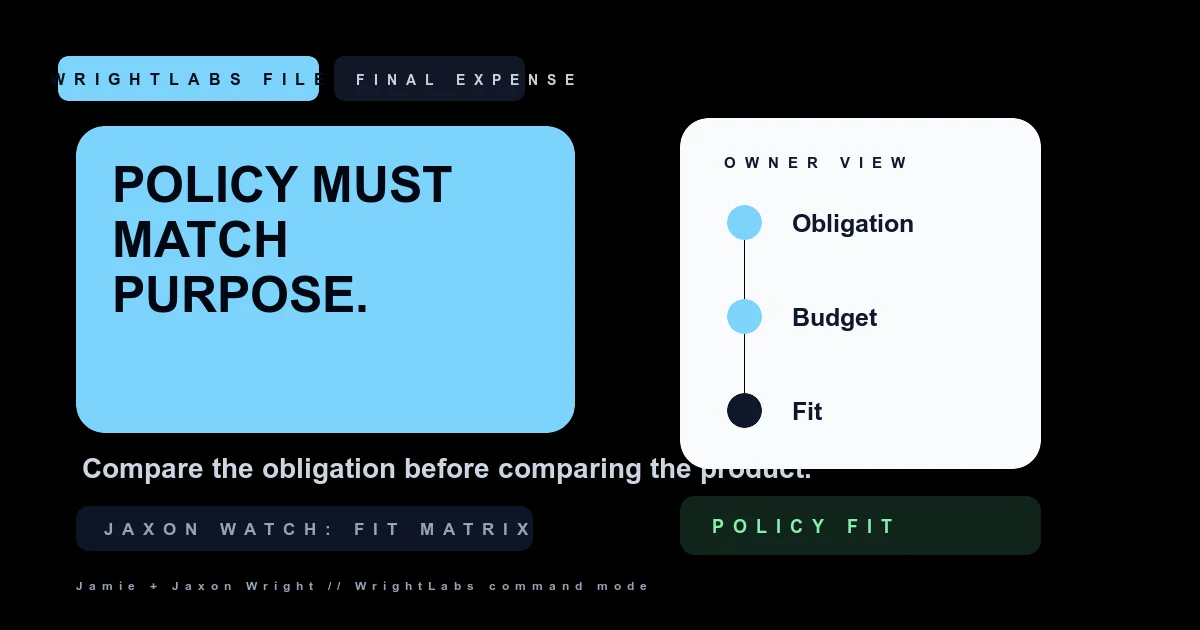

The policy should match the obligation, not the other way around.

The WrightLabs system view

Ask what the coverage should pay for, how long it must last, health constraints, monthly budget, beneficiary goals, and whether cash value matters. This is where the FMO Command OS philosophy matters: build the workflow around the decision the owner or manager needs to make, then let the automation serve that decision.

In practice, the life policy comparison intake has five jobs. First, it captures the event cleanly. Second, it enriches the record with context. Third, it decides whether the next move is AI, human, or both. Fourth, it writes the result back to the CRM. Fifth, it reports the outcome in language an operator can use on Monday morning.

For the insurance-operator side of the system, the FMO Command OS shows how WrightLabs structures permissioned intake, routing, and manager visibility. The WrightLabs GHL MCP is the control layer for governed CRM actions, while Proof gives examples of the operating style behind these recommendations. Browse the full operator brief for the rest of this sprint.

| Operating point | Weak version | WrightLabs standard |

|---|---|---|

| Purpose | End-of-life costs | Lifelong protection and broader planning |

| Coverage size | Often smaller | Often larger |

| Underwriting | Often simplified | Can be more detailed |

| Cash value | May exist but smaller | Often a larger feature |

The workflow to build first

Start with a narrow workflow before trying to automate the whole business. A narrow workflow is easier to QA, easier to explain to staff, and easier to improve. The first build should make one promise that the team can inspect: a lead is captured, classified, routed, followed up, and reported without disappearing into a personal inbox.

For this topic, WrightLabs would start with a trigger, a context package, an action policy, and a stop condition. The trigger says what starts the workflow. The context package says what the AI or human must know. The action policy says what the system may do. The stop condition says when the workflow is finished, escalated, or suppressed.

life policy comparison intake

trigger: new inquiry, reply, call event, or stale-stage timer

context: source, contact, status, timeline, consent, owner, and last touch

action: classify, summarize, route, message, task, or escalate

stop: booked, disqualified, opted out, human review, or nurtureThe point of this structure is accountability. If a manager asks why the record moved, the answer should be visible in the contact note, the stage history, and the dashboard. If a customer or prospect says stop, the system should stop. If a rep needs context, the handoff should show the reason for the handoff, not just a mysterious task.

Metrics, risks, and guardrails

Final expense content converts when it treats the reader like a family planner, not a policy shopper. A good metric is not just something that makes a chart look alive. It should help an operator choose a fix: change routing, rewrite the first message, adjust staffing, clean a data source, or remove a workflow that creates noise.

The highest-risk version of final expense vs whole life insurance is the version that hides assumptions. If the workflow assumes consent, assumes the right owner, assumes a plan type, assumes a service area, or assumes a rep followed up, the system will eventually create a bad handoff. The better version makes those assumptions visible and reviewable.

Final expense content converts when it treats the reader like a family planner, not a policy shopper.

Owner checklist

- Start with the expense you want covered.

- Compare total cost over time.

- Do not ignore health and underwriting constraints.

- Make the owner-visible metric match the real business outcome, not the easiest field to chart.

- Review low-confidence AI actions weekly until the workflow is stable.

How to turn this into qualified traffic

This post is part of a two-track WrightLabs SEO system. Track one attracts GHL operators, home-service owners, and agency builders who need implementation help now. Track two attracts Medicare, FMO, life-insurance, and turning-65 traffic that can feed advisor workflows, content engines, and compliant follow-up systems.

The business value is in the bridge between education and execution. A reader who understands final expense vs whole life insurance should be able to see the workflow gap in their own operation. The page should not ask them to buy a vague AI product. It should invite them into a concrete build conversation about the workflow, dashboard, or front desk system that fixes the leak.

The implementation note is simple: make one source of truth before adding more channels. If contacts, calls, forms, messages, agent tasks, and manager notes live in different places, every new automation multiplies the confusion. If those signals land in one governed CRM path, AI can help summarize, route, and recover work without becoming another disconnected tool for the team to babysit.

Final Expense vs Whole Life Decision Sheet

Compare coverage job, premium fit, underwriting, cash value, family needs, and senior-policy constraints. Match the policy type to the obligation it is supposed to cover.

For a related operating angle, read How Much Term Life Insurance Do I Need and Medicare Advantage vs Medicare Supplement. Those posts connect this topic to the broader WrightLabs architecture.

FAQ

Bottom line

Comparison plus who each fits. The move is to make the workflow specific enough to inspect and simple enough for the team to trust. If the system improves speed, routing, compliance context, or manager visibility, it can turn search traffic into a real sales conversation instead of another pageview.